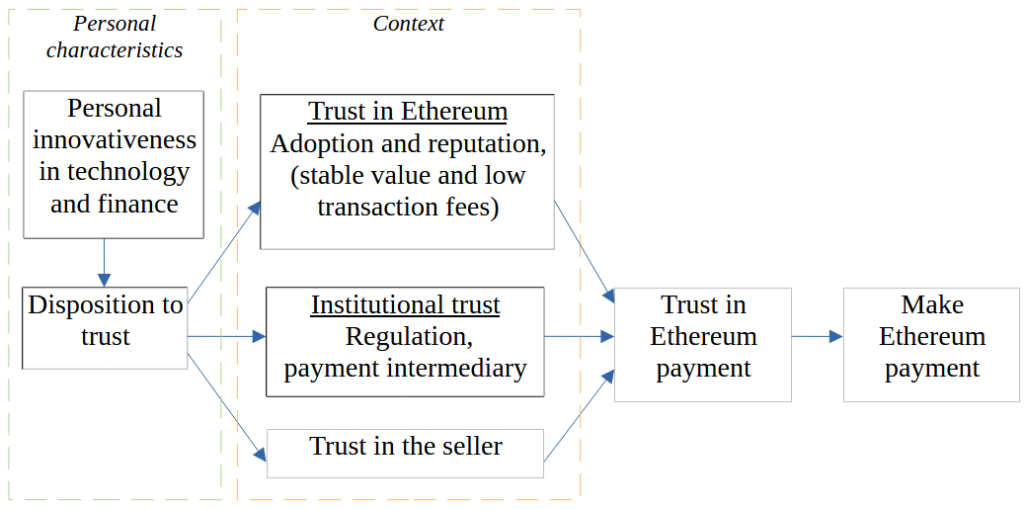

My new research developed a model of trust in making payments with the Ethereum (Zarifis, 2023). I published the first peer reviewed research on trust in payments with Bitcoin in 2014 (Zarifis et al. 2014), and I wanted to apply my experience from that to understanding the consumer’s perspective to making Ethereum payments.

Ethereum is being utilised in various ways, including smart contracts and payments. Despite some similarities with Bitcoin, Ethereum is a different technology, with different governance and support.

Ethereum payments require digital wallets and the process is different to paying in traditional fiat currencies like the Euro. When a person wants to take an action without controlling all the parameters, and some risk is unavoidable, trust is necessary.

Figure 1. Model of trust in making Ethereum payments, TRUSTEP

The model demystifies how trust is built in consumer payments with Ethereum. The model starts with the individual’s predisposition and then covers the factors from the specific context of Ethereum payments. From the person’s individual characteristics, their willingness to innovate in finance and technology have a role. There are then five variables from the contexts: Adoption and reputation, stable value and low transaction fees, effective regulation, payment intermediaries and trust in the seller. The personal and contextual factors together influence trust in the Ethereum payment process and making a payment with Ether.

While the model has similarities to previous models of trust, such as the role of each individual’s psychological predisposition and the role of reputation, the role of institutions such as regulators and the importance of trust in the retailer, the distinct characteristics of Ethereum also play a role. In fact, the factors related to the distinct characteristics of Ethereum have the strongest support based on the average of the responses. This research can be added to a growing body of research in trust that illustrates how users’ beliefs in each cryptocurrency need to be explored separately.

Furthermore, the role of the organizations involved in the payment process are shown. While trust in the retailer is usually a factor in retail payments, the regulators and payment intermediaries are not always a significant factor, so it is a useful contribution to show that this is the case here.

That is what I want to share with you here. If you have experiences related to what I am talking about, please let me know, I would love to hear from you.

Reference

Zarifis A. (2023) ‘A Model of Trust in Ethereum Token ‘Ether’ Payments, TRUSTEP’, Businesses, vol.3, no. 4: pp.534-547. https://doi.org/10.3390/businesses3040033 (open access)

Zarifis A., Efthymiou L., Cheng X. & Demetriou S. (2014) ‘Consumer trust in digital currency enabled transactions’, Lecture Notes in Business Information Processing-Springer, vol.183, pp.241-254. http://link.springer.com/chapter/10.1007/978-3-319-11460-6_21#

Please sign this petition for the editor to credit me for my work, by replying to this post or sending me a private message. This is a short overview of what happened to the best of my understanding:

I was given the task by a lecturer of UCLAN I had worked with in the past (I hired her for her first academic job) to turn a good student dissertation into a research paper. I am often given the task of turning research into a paper because my first language is English and I have a decent record at getting papers published.

It took many hours to turn it into a paper, I identified the most valuable parts and wrote several sections of the final paper. For example I strengthened the link to trust which is my specialist subject. The paper was published in a journal in 2018. The first author credited on the paper is the student, then the two supervisors from UCLAN and lastly me. I have an email from one of the co-authors from UCLAN expressing her gratitude for the publication and stating that based on the work I did, my name should not have been last on the list but further up.

In 2020 I came across the same paper published in a different journal, without my name as co-author. I contacted the editor and told him the paper is already published and not retracted when it was published a second time. Based on the ethics guidelines of the journal there were two options available to the editor as I understand it:

a) Based on the ethics guidelines of the journal, credit the author that was left out as he has the best evidence imaginable that he is a co-author, and the corresponding author belatedly acknowledged he should be credited. (I also have several emails, drafts etc. as evidence)

b) Based on the ethics guidelines of the journal, retract the paper the editor published in his journal because it was published before and not retracted.

He did not act on the evidence that the paper is already published, waited for the corresponding author to retract the original paper and then said he could not take into account the original version, despite it being published at the time it was published again, and only retracted when the co-author left out, used it as evidence. (the original paper has already been cited several times and is still widely available)

I contacted the corresponding author from UCLAN and he said in writing (I have the email) that he would ask the editor to add me and if the editor did not agree he would add me as co-author on another paper to make up for the mistake. Neither happened.

I have several emails, drafts and a published paper, that was not retracted when it was published a second time, that has been cited several times, proving irrefutably I am a co-author of that paper.

Neither the editor, the publisher or the co-authors have taken action to correct this. The action that has been taken so far is for some people to contact my work to try to make my life harder.

Please sign this petition for the editor to credit me for my work. You can sign the petition by replying to this article or sending me a private message with your name and if you want your affiliation.

Evidence

I provide here a small subset of the evidence, the papers that cite the original publication with me as co-author. If anyone wants to see the emails that prove everything I have said, I can show them.

Here is the citation of the original paper:

Michael P., Dimitriou S., Glyptis L. & Zarifis A. (2018) ‘e-Government implementation challenges in developing countries: The project manager’s perspective’, International Journal of Public Administration and Management Research (IJPAMR), vol.4, no.3, pp.1-17. Available from: http://www.rcmss.com/index.php/ijpamr

The original publication was published and not retracted for over two years before this:

‘Glyptis L., Christofi M., Vrontis D., Del Giudice M., Dimitriou S, Michael P. (2020) ‘E-Government implementation challenges in small countries: The project manager’s perspective’, Technological Forecasting and Social Change’

Here are some people that cited the original paper with me as a co-author:

An e-government implementation framework: A developing country case study A Apleni, H Smuts – Responsible Design, Implementation and Use of …, 2020 – Springer The implementation of Information and Communication Technology (ICT) is seen globally as a means to efficient and effective delivery of business and organisational mandates …

The role of political will in enhancing e-government: An empirical case in Indonesia SY Defitri – Probl. Perspect. Manag, 2022 – businessperspectives.org E-government is an issue that is widely discussed by several studies because it has an impact on improving government performance. Weak political will of the heads of state and …

Quality Evaluation of E-Government Services–The Case of Albania R Keco, I Tomorri, K Tomorri – Transylvanian Review of Administrative …, 2023 – rtsa.ro QUALITY EVALUATION OF E-GOVERNMENT SERVICES – THE CASE OF ALBANIA Remzi KECO Ilir TOMORRI Kejsi TOMORRI Page 1 20 Abstract Albania has passed a period of three …

Analysis of Information System Audit Using Control Objectives for Information and Related Technology 5 Framework on Permata Hebat Application MS Muryantoro, DA Efrilianda – Journal of Advances in …, 2023 – journal.unnes.ac.id Permata Hebat application is an application created as a service to develop micro businesses among housewifes in Semarang City. However, to fulfill this expectation, of …

Challenges in E-governments: A case study-based on Iraq NA Jasim, EM Hameed, SA Jasim – IOP Conference Series …, 2021 – iopscience.iop.org An effective and competent way to deliver business and organizational mandates is via deploying Information and Communication Technology (ICT). Parts of a government’s job is …

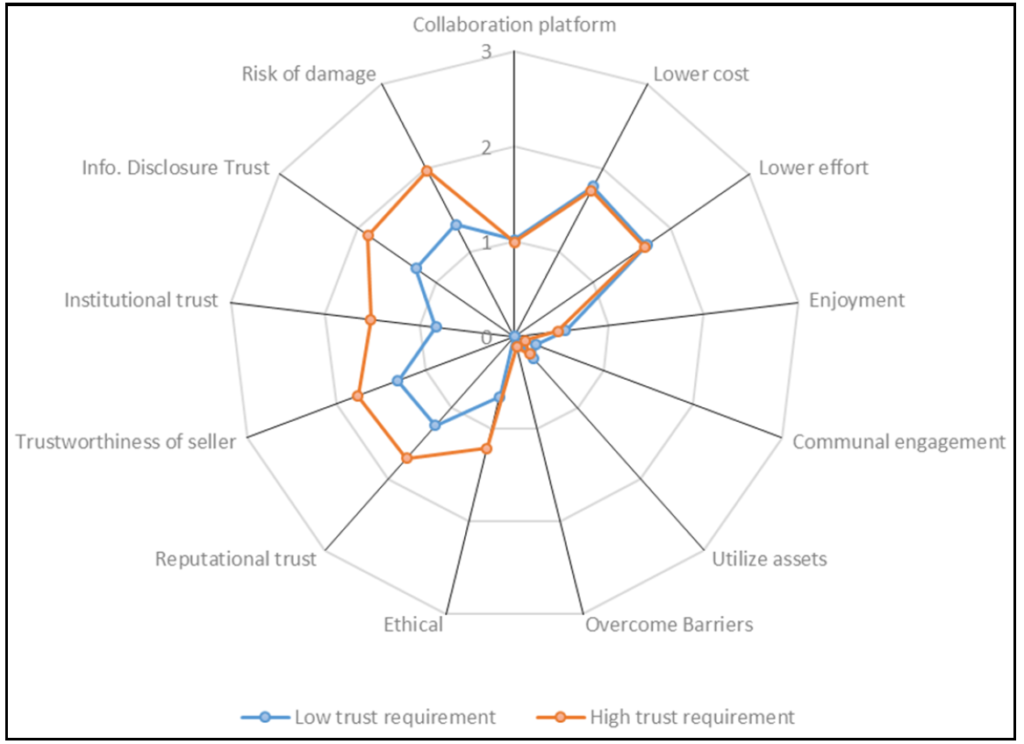

Collaborative Consumption (CC) and the sharing economy, where consumers do not purchase a product or service, but share it, is growing in popularity. This is due to a trend away from ownership towards experiencing. The first two areas of the economy that this business model disrupted were fare sharing and renting rooms for short periods. Other areas are also influenced but it is unclear which sectors of the economy will be disrupted next. Smaller niches of the economy, or areas where more public-sector involvement is necessary, such as the elderly and the disabled may not be at the forefront and may be the laggards losing out on possible benefits for years.

This research evaluates the current CC business models and identifies 13 ways they add value from the consumer’s perspective. This research further explores whether CC business models fall into two categories in terms of what the consumer values. In the first category, they require a low level of trust while in the second category a higher level of trust is necessary. Our survey evaluates whether there was a difference between CC business models that require a low level of trust such as a taxi service and those that required a high level of trust such as supporting the elderly and disabled.

Figure 1. Comparative spider diagram of value added by collaborative consumption business models for low and high required trust

The analysis verified that the consumer requires 13 types of value added from the business model which can be separated into three categories which are personal interest, communal interest and trust building. It is important for organizations to acknowledge how they relate to these dimensions.

It was found that CC business models can be separated into those that require a relatively low level of trust such as fare sharing and those that require a high level of trust such as supporting the elderly and disabled, as we can see in the figure here. For the business models that only require low trust, the consumer considered the personal interest value added more important, while in the those requiring more trust the consumer rated the value added of trust building higher.

The findings suggest that changing CC business model from one that requires low trust to one that requires higher trust necessitates a significant improvement in how the organisation builds trust. This can be considered a ‘step’ change in trust-building which would have to be a consideration at business model level. Iterative improvements at operational level may not increase trust sufficiently.

Reference

Zarifis A., Cheng X. & Kroenung J. (2019). Collaborative consumption for low and high trust requiring business models: From fare sharing to supporting the elderly and disabled, International Journal of Electronic Business, vol.15, no.1, pp.1-20. https://www.inderscienceonline.com/doi/abs/10.1504/IJEB.2019.099059 (open access)

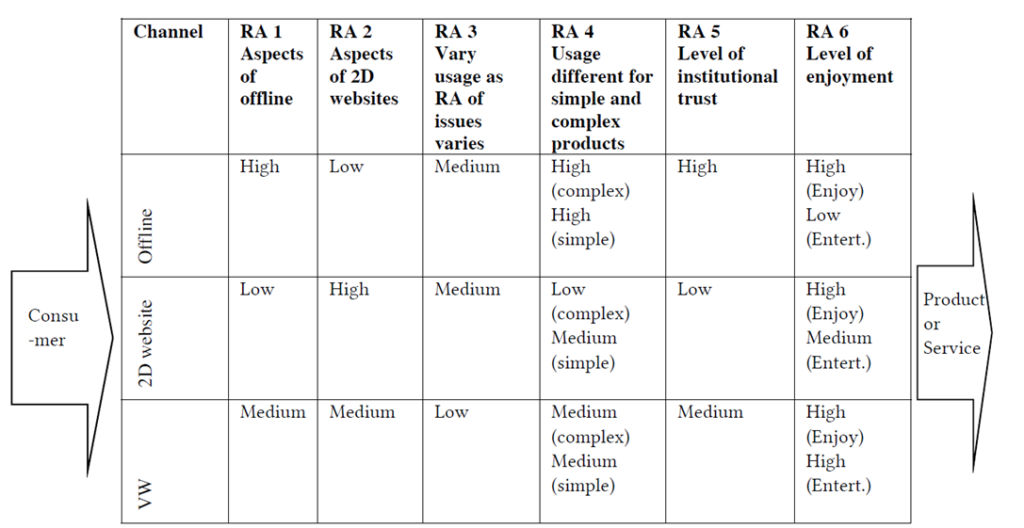

Have you made a purchase from a three dimensional Virtual World (VW)? Probably not, only a small minority have. When VWs first became popular fifteen years ago, people jumped to the conclusion that they were the future, the new platform to socialise online. Their adoption however did not end up being exponential. So why do the experts often think VWs, with their additional functionality are the future, but that future has not come yet? We decided to ask the consumer. There is a degree of understanding on what each channel can offer but the relative advantage of each channel in relation to the others is less understood. By relative advantage we mean something the one channel, for example three dimensional VWs, have an advantage over two dimensional, traditional, websites. This research, evaluates the relative advantage between the channels of three-dimensional VWs, two-dimensional websites, and offline retail shops. The consumer’s preferences across the three channels, were distinguished across six relative advantages.

Figure 1 The three channels and six relative advantages in multichannel retail In the figure, you can see at the top the six different relative advantages, and beneath them, how the three different channels perform, in relation to these relative advantages. Participants, showed a preference for offline and 2D websites, in most situations apart from enjoyment, entertainment, sociable shopping, the ability to reinvent yourself, convenience and institutional trust where the VWs were preferred. We can look in more detail at the fifth relative advantage, that VWs have higher institutional trust compared to 2D websites. Consumers value the role of the VW as an institution in relation to trust. One feature that is appreciated is that the buyer does not receive your banking details. Some participants value the role of the VWs administration in identifying and warning about specific threats. The findings illustrated in the figure, show that the consumer’s preference varies across the three channels, and six RAs. An organization pursuing a multichannel strategy, can adapt their offerings in each channel to fully utilize these different preferences. While on most issues VWs are the least appealing from the three channels, framing the comparison with the six relative advantages shows how they have a useful and complementary role to play in multichannel retail. For example, customer support can be done in VWs. An organization, can use these findings to shape their business model and strategy.

Reference Zarifis A. (2019) ‘The six relative advantages in multichannel retail for three-dimensional Virtual Worlds and two-dimensional websites’, Proceedings of the 10th ACM Conference on Web Science, June 19–21, Boston, USA, pp.363-372. https://dl.acm.org/doi/pdf/10.1145/3292522.3326038

Several countries’ economies have been disrupted by the sharing economy. However, each country and its consumers have different characteristics including the language used. When the language is different does it change the interaction? If we have a discussion in English and a similar discussion in German will it have the same meaning exactly, or does language lead us dawn a different path? Is language a tool or a companion holding our hand on our journey?

This research compares the text in the profile of those offering their properties in England in English, and in Germany in German, to explore if trust is built, and privacy concerns are reduced, in the same way.

Figure 1. How landlords build trust in the sharing economy

The landlords make an effort to build trust in themselves, and the accuracy of the description they provide. The landlords build trust with six methods: (1) The first is the level of formality in the description. More formality conveys a level of professionalism. (2) The second is distance and proximity. Some landlords want to keep a distance so it is clear that this is a formal relationship, while others try to be more friendly and approachable. (3) The third is ‘emotiveness’ and humour, that can create a sense of shared values. (4) The fourth method of building trust is being assertive and passive aggressive, that sends a message that the rules given in the description are expected to be followed. (5) The fifth method is conformity to the platform language style and terminology that suggests that the platform rules will be followed. (6) Lastly, the sixth method to build trust is setting boundaries that offer clarity and transparency.

Privacy concerns are not usually reduced directly by the landlord as this is left to the platform. The findings indicate that language has a limited influence and the platform norms and habits have the largest influence. We can say that the platform has choreographed this dance sufficiently between the participants so that different languages have a limited influence on the outcome.

Reference

Zarifis A., Ingham R. & Kroenung, J. (2019) ‘Exploring the language of the sharing economy: Building trust and reducing privacy concern on Airbnb in German and English’, Cogent Business & Management, vol.6, iss.1, pp.1-15. https://doi.org/10.1080/23311975.2019.1666641 (open access)

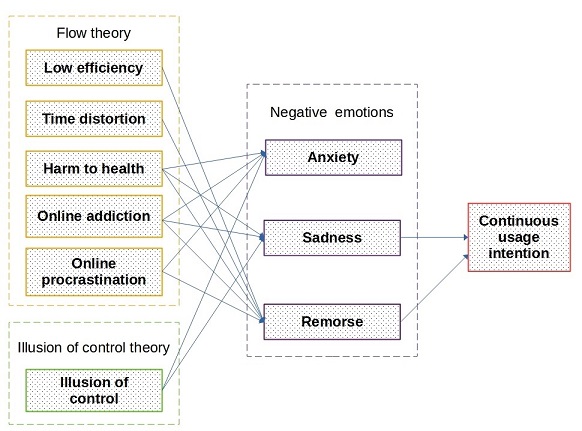

Short videos are very popular but if they take up a-lot of people’s time, they gradually change people’s living habits. Therefore it is useful to understand the negative implications of short videos. The results show that users’ viewing many short videos can have negative emotions, and these negative emotions can affect users’ intention to continue to use short video platforms. The model developed in this research shows that there are three negative emotions caused by six factors. Two of these three negative emotions then influence the intention to continue using short videos.

Fig 1. Model of users’ negative emotions and continuous usage intention in short video platforms

From the six factors that cause negative emotions, the five are related to flow theory. Flow theory is relevant here because watching short videos is a flow experience. Flow theory is a state where someone is fully immersed in an activity, they are enjoying it and other things do not seem to matter as much.

The first of the five factors related to flow theory is the low efficiency the user has in their work and other tasks, due to watching short videos. The second is time distortion, meaning that the users perception of time is not as accurate during this activity. What might feel like a short amount of time can be much longer. The third is the harm to their health. Both mental and physical health can be harmed by spending a long time watching short videos. The fourth is the online addiction they experience, making them want to keep watching the short videos. The fifth is online procrastination, making the user watch more short videos to delay working and making decisions related to their work.

The sixth factor that can cause negative emotions is illusion of control. The theory of illusion of control suggests that in some situations a person can be overconfident about their control of a situation. A person can have a level of optimism that they will get the outcome they want, that is unrealistic. The negative emotions include anxiety, sadness and remorse. The research found strong support that sadness and remorse influence the users intention to continue using the short videos.

Reference: Cheng X., Su X., Yang B., Zarifis A. & Mou J. (2023) ‘Understanding users’ negative emotions and continuous usage intention in short video platforms’, Electronic Commerce Research and Applications, vol.58, 101244, pp.1-15. https://doi.org/10.1016/j.elerap.2023.101244

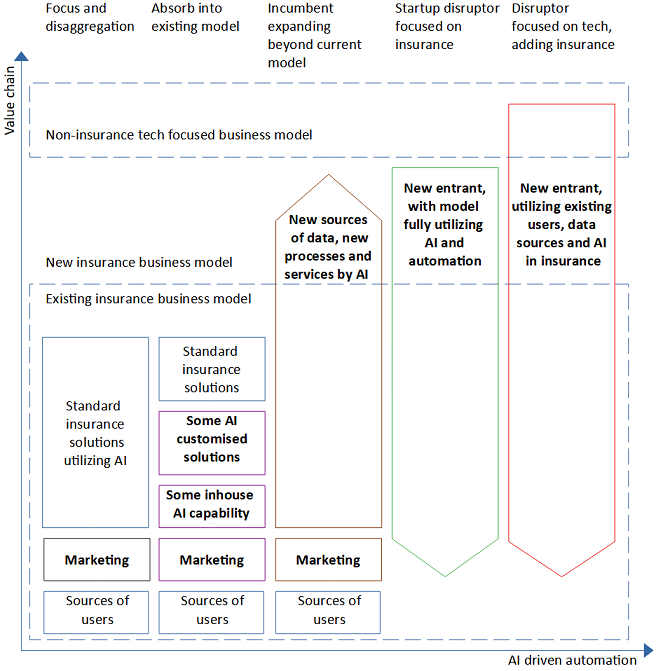

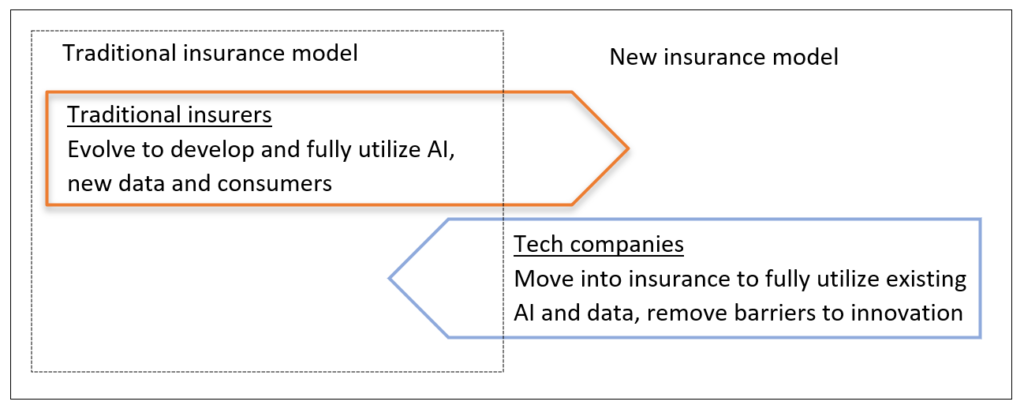

Artificial intelligence (AI) and related technologies are creating new opportunities and challenges for organizations across the insurance value chain. Incumbents are adopting AI-driven automation at different speeds, and new entrants are attempting to use AI to gain an advantage over the incumbents. This research explored four case studies of insurers’ digital transformation. The findings suggest that a technology focused perspective on insurance business models is necessary and that the transformation is at a stage where we can identify the prevailing approaches. The findings identify the prevailing five insurance business models that utilize AI for growth: (1) focus on a smaller part of the value chain and disaggregate, (2) absorb AI into the existing model without changing it, (3) incumbent expanding beyond existing model, (4) dedicated insurance disruptor, and (5) tech company disruptor adding insurance services to their existing portfolio of services (Zarifis & Cheng 2022).

Figure 1. Updated model of five business models in insurance with disruptors split into two types

In addition to the five business models illustrated in Figure 1, this research identified two useful avenues for further exploration: Firstly, many insurers combined the two first business models. For some products, often the simpler ones, such as car insurance, they focused and disaggregated. For other parts of their organization, they did not change their model, but they absorbed AI into their existing model. Secondly, new entrants can be separated into two distinct subgroups: (4) disruptor focused on insurance and (5) disruptor focused on tech but adding insurance.

New Fintech and Insurtech services are popular with consumers as they offer convenience, new capabilities and in some cases lower prices. Consumers like these technologies but do they trust them? The role of consumer trust in the adoption of these new technologies is not entirely understood. From the consumer’s perspective, there are some concerns due to the lack of transparency these technologies can have. It is unclear if these systems powered by artificial intelligence (AI) are trusted, and how many interactions with consumers they can replace. There have been several adverts recently that emphasize that their company will not force you to communicate with AI and will provide a real person to communicate with are evidence of some push-back by consumers. Even pioneers of AI like Google are offering more opportunities to talk to a real person an indirect acknowledgment that some people do not trust the technology. Therefore, this research attempts to shed light on the role of trust in Fintech and Insurtech, especially if trust in AI in general and trust in the specific institution play a role (Zarifis & Cheng, 2022).

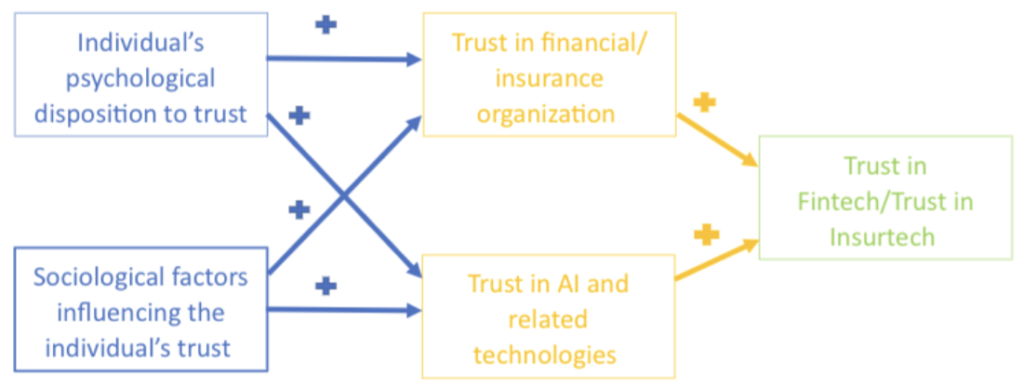

Figure 1. A model of trust in Fintech/Insurtech

This research validates a model, illustrated in figure 1, that identifies the four factors that influence trust in Fintech and Insurtech. As with many other models of human behavior, the starting point is the individual’s psychology and the sociology of their environment. Then, the model separates trust in a specific organization and trust in a specific technology like AI. This is an important distinction: Consumers have beliefs about the organization they bring with them and other pre-existing beliefs on AI. Their beliefs on AI might have been shaped by experiences with other organizations.

Therefore, the validated model shows that trust in Fintech or Insurtech is formed by the (1) individual’s psychological disposition to trust, (2) sociological factors influencing trust, (3) trust in either the financial organization or the insurer and (4) trust in AI and related technologies.

This model was initially tested separately for Fintech and Insurtech. In addition to validating a model for trust in Fintech and Insurtech separately, the two models were compared to see if they are equally valid or different. For example, if one variable is more influential in one of the two models, this would suggest that the model of trust in one of them is not the same as in the other. The results of the multigroup analysis show that the model is indeed equally valid for Fintech and Insurtech. Having a model of trust that is suitable for both Fintech and Insurtech is particularly useful as these services are often offered by the same organization, or even the same mobile application side by side.

Reference

Zarifis A. & Cheng X. (2022) ‘A model of trust in Fintech and trust in Insurtech: How Artificial Intelligence and the context influence it’, Journal of Behavioral and Experimental Finance, vol. 36, pp. 1-20. https://doi.org/10.1016/j.jbef.2022.100739 (open access)

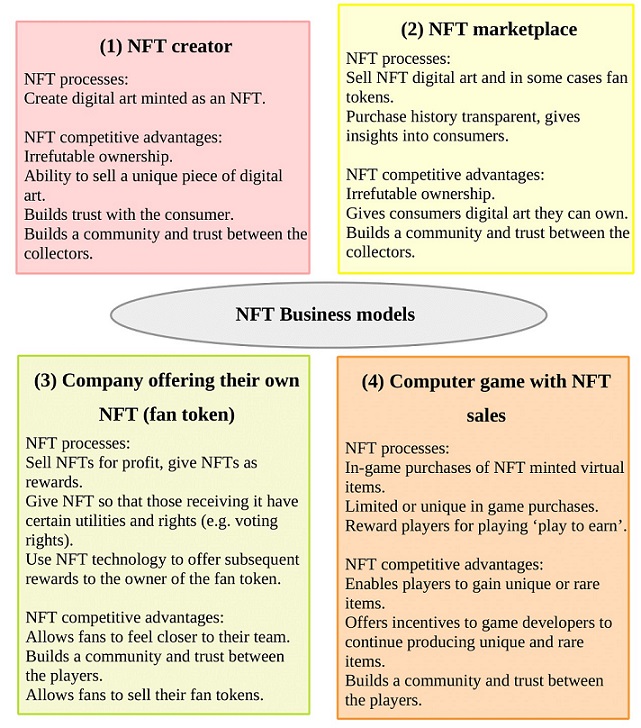

The interest in Non-fungible Tokens (NFTs) has ‘exploded’ recently, but it is not clear what final form they will take. This innovation will have difficulties reaching a wider audience until more clarity is achieved on two main issues: What exactly are the NFT business models, and how do they build trust. The findings of recent research (Zarifis and Cheng, 2022), illustrated in figure 1, show that there are four NFT business models:

(1) The first business model is an NFT creator: They can create digital art that is then minted as an NFT, and sold on an NFT platform. The NFT competitive advantages include having proof of irrefutable ownership, and the ability to sell a piece of art that is unique or limited to a low number. The reliability and transparency of the NFT, build trust with the consumer.

Figure 1: The four NFT business models

(2) The second business model is an NFT marketplace, selling creators’ NFTs: The competitive advantage of NFTs as part of this business model is once again the irrefutable ownership, and that it gives consumers digital art they can own. The purchase history of the consumers is transparent, so this gives insights into their interests. As with the previous business model, a community and trust are built between the collectors.

(3) The third business model is a Company offering their own NFT, typically a fan token: This business model has several NFT processes. These are to sell NFTs for profit, to give NFTs as rewards, make payment with fan tokens, give an NFT so that the person receiving it has certain utilities and rights, such as voting rights. The competitive advantages of NFTs, within this business model, are that they allow fans to feel closer to their team and builds a community and trust between the fans.

(4) The fourth business model is a Computer game with NFT sales: There can be in-game purchases of NFT minted virtual items, limited or unique in game purchases and players can be rewarded for playing, know as ‘play to earn’. This offers incentives to game developers to continue producing rare items, provides an ongoing revenue stream for existing games, and builds a community and trust between the players.

This research was the basis of Dr Alex Zarifis keynote speech in front of around 300 people at the 2022 JEBDE’s 2nd Academic Conference on Electronic Business & Digital Economics on the 28/09/22.

Reference

Zarifis A. & Cheng X. (2022) ‘The business models of NFTs and Fan Tokens and how they build trust’, Journal of Electronic Business & Digital Economics, vol.1, pp.1-14. https://doi.org/10.1108/JEBDE-07-2022-0021

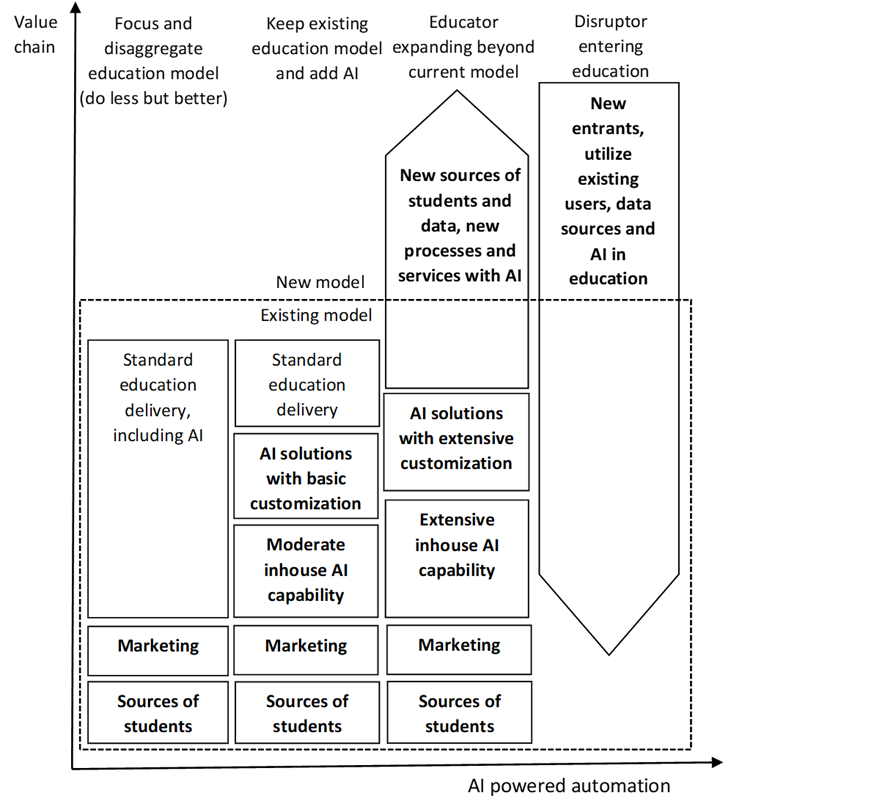

Universities, like many other organizations, are going through a disruptive digital transformation. The alure of AI and automation, allowing smarter, more responsive and scalable universities is clear. What is less clear is what a university will look like five years into this process. We identified four business models that can give leaders a destination for the digital transformation journey (Zarifis and Efthymiou 2022):

(1) This first education business models that is optimized for AI is to focus and disaggregate: In addition to the classroom the successful delivery of education requires a supply chain. With the changes in this supply chain caused by AI an educator can chose to focus on one part of this supply chain. They can focus on the part of the supply chain where their skills are best suited and build an ecosystem for the rest.

Figure 1. Four education business models that are optimised for AI (adapted from (Zarifis, Holland, and Milne 2019))

(2) The second model that is optimized for AI is to keep the existing education model and add AI: Despite the transformational nature of AI, some universities use AI to make the existing model more effective without changing it fundamentally. This may involve more back-office AI applications and less student facing applications.

(3) The third education model that is optimized for AI is an educator expanding beyond the current model: In this model the educator takes advantage of new opportunities emerging from AI and digital transformation. The educator keeps their existing part of the education supply chain, but they also add new processes that take advantage of AI to reach more students and more data.

(4) The fourth model that is optimized for AI is the model of a disruptor entering education: As technology plays a more decisive role in many areas, including education, tech savvy companies can use their advanced systems and existing user base and add other new services. Education can be added as a new feature to a platform in a similar way that banking and insurance services have been added.

The four models presented give a strategic direction and make it easier for the leader of the digital transformation to communicate it. The leader of digital transformation will have to make many choices along this journey, so it is important that all the decisions are compatible with the chosen education business model.

References

Zarifis A. & Efthymiou L. (2022) ‘The four business models for AI adoption in education: Giving leaders a destination for the digital transformation journey’, IEEE Global Engineering Education Conference (EDUCON), pp.1866-1870. https://doi.org/10.1109/EDUCON52537.2022.9766687

Zarifis A., Holland C.P. & Milne A. (2019) ‘Evaluating the impact of AI on insurance: The four emerging AI and data driven business models’, Emerald Open Research, pp.1-17. https://emeraldopenresearch.com/articles/1-15/ (open access)

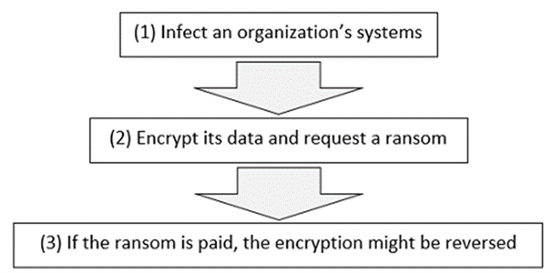

Ransomware attacks are not a new phenomenon, but their effectiveness has increased causing far reaching consequences that are not fully understood. The ability to disrupt core services, the global reach, extended duration, and the repetition of these attacks has increased their ability to harm an organization.

One aspect that needs to be understood better is the effect on the consumer. The consumer in the current environment, is exposed to new technologies that they are considering to adopt, but they also have strong habits of using existing systems. Their habits have developed over time, with their trust increasing in the organization in contact directly, and the institutions supporting it. The consumer now shares a significant amount of personal information with the systems they have a habit of using. These repeated positive experiences create an inertia that is hard for the consumer to move out of. This research explores whether the global, extended, and repeated ransomware attacks reduce the trust and inertia sufficiently to change long held habits in using information systems. The model developed captures the cumulative effect of this form of attack and evaluates if it is sufficiently harmful to overcome the e-loyalty and inertia built over time.

Figure 1. The steps of a typical ransomware attack

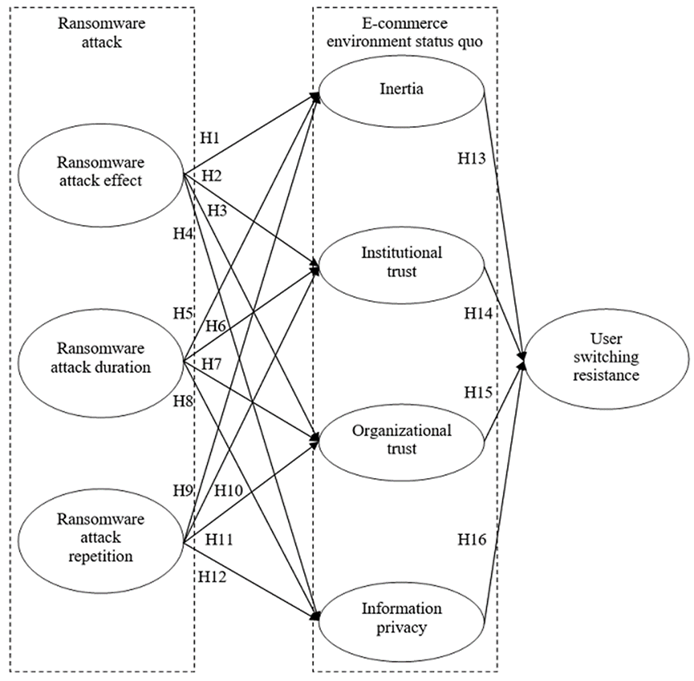

This research combines studies on inertia and resistance to switching systems with a more comprehensive set of variables that cover the current e-commerce status quo. Personal information disclosure is included along with inertia and trust as it is now integral to e-commerce functioning effectively.

As you can see in the figure the model covers the 7 factors that influence the consumer’s decision to stop using an organization’s system because of a ransomware attack. The factors are in two groups. The first group is the ransomware attack that includes the (1) ransomware attack effect, (2) duration and (3) repetition. The second group is the E-commerce environment status quo which includes (4) inertia, (5) institutional trust, (6) organizational trust and (7) information privacy.

Figure 2. Research model: The impact of ransomware attacks on the consumer’s intentions

The implications of this research are both theoretic and practical. The theoretic contribution is highlighting the importance of this issue to Information Systems and business theory. This is not just a computer science and cybersecurity issue. We also linked the ransomware literature to user inertia in the model.

There are three practical implications: Firstly, by understanding the impact on the consumer better we can develop a better strategy to reduce the effectiveness of ransomware attacks. Secondly, processes can be created to manage such disasters as they are happening and maintain a positive relationship with the consumer. Lastly, the organizations can develop a buffer of goodwill and e-loyalty that would absorb the negative impact on the consumer from an attack and stop them reaching the point where they decide to switch system.

Dr Alex Zarifis presenting research on ransomware

References

Zarifis A., Cheng X., Jayawickrama U. & Corsi S. (2022) ‘Can Global, Extended and Repeated Ransomware Attacks Overcome the User’s Status Quo Bias and Cause a Switch of System?’, International Journal of Information Systems in the Service Sector (IJISSS), vol.14, iss.1, pp.1-16. Available from (open access): https://doi.org/10.4018/IJISSS.289219

Zarifis A. & Cheng X. (2018) ‘The Impact of Extended Global Ransomware Attacks on Trust: How the Attacker’s Competence and Institutional Trust Influence the Decision to Pay’, Proceedings of the Americas Conference on Information Systems (AMCIS), pp.2-11. Available from: https://aisel.aisnet.org/amcis2018/Security/Presentations/31/

Most of us appreciate the importance of Artificial Intelligence (AI) and we know it is bringing big changes. Will we finally have that robot assistant we were promised 50 years ago? Will we even have to work, at least in the sense of how we view work today? It is fun to daydream about these things, but insurers need some certainty on what the future looks like. Some new insurers are trying new business models enthusiastically and then changing direction sharply, like a speedboat swerving to avoid a collision. The larger insurers, however, are like large cruise ships. They need to be able to see far ahead before they plot their course, and they don’t want to keep changing direction.

We wanted to identify the viable AI driven business models to help give some clarity and guidance. Previous efforts had identified four models being applied now, that showed a varying level of enthusiasm for AI. But what about ten years from now? Would there be convergence to one model? If not, what are the key issues stopping this?

AI is bringing fundamental changes to insurance business models. Those that fail to adapt are likely to disappear. Some traditional insurers are trying to just be more effective with AI, while others reinvent themselves to fully utilize the new capabilities available. Tech-savvy companies from outside the sector like Tesla, are entering and disrupting it. Despite these diverging approaches, there are signs of a convergence towards one, ideal, business model.

Our research focused on one example of a traditional insurer and one new tech-savvy disruptor and evaluated whether their models are converging. We found a high degree of convergence, but some differences are likely to remain even after this transitionary period.

Table 1. Traditional insurers and tech companies AI powered insurance business models

Difference

Traditional insurer

Tech company offering insurance

Service and revenue

Complex and simple service, B2B and B2C Improve customization and interaction

Simple standardised B2C services Revenue not a priority

Estimating risk and pay-outs

Information of a high relevance, quality, and reliability

Real time information on behavior Proactively influence behavior and reduce risk

Consumer interaction

Several business models in parallel to utilize different technologies Alliance with tech companies to access their user base Better automated interaction

Bundle insurance with existing services, remove the hurdle of insurance for the consumer Use existing access to user data so no additional privacy concerns

AI is changing the insurance value chain, as illustrated in figure 1. Most new insurers, like Tesla, offer fully automated simple services. The traditional insurers offer some of their simpler services in this way. The more complex services are supported with AI, but a human makes the final decision. An example of this are audits for fraud, where the AI identifies unusual patters and cases for an expert to evaluate.

Figure 1. Convergence of traditional and new, disrupting insurers

There are signs of convergence between the models of traditional and new insurers. First, there is convergence in technologies, such as the use of chatbots utilizing AI. Second, there is a convergence in processes, for example, the interaction with the consumer. Third, there is convergence in the strategy on costs and pricing.

However, there are two areas where there seems to be a limit on convergence, which seems to suggest the business models of the incumbent and the disruptor will remain distinct. These are: (1) evaluating risk and (2) the cost of attracting the user and profitability.

Evaluating Risk

AI is changing the way risk is evaluated by an insurer. These new ways of using data and technology to assess risk, in turn generate new insurance services. This is true for new insurers but also some forward-looking traditional insurers. Some existing insurers are creating new services from the new data that is available to them, but they are also creating new services to gain new data.

New insurers like Tesla calculate risk in three ways. First, data is collected from the cameras and sensors in the vehicle providing insight on real time behavior of individuals and groups. Second, a broader analysis of individuals with hundreds of variables is implemented and new algorithms that evaluate risk accurately are improved. Third, the impact on risk of the new technologies is constantly monitored and, in some cases, influenced. For example, software upgrades can be made instantly to all vehicles to improve safety.

Cost of Attracting the User and Profitability

The technology company offering insurance has some advantages in terms of the cost of attracting new consumers and the profits they generate. While the traditional insurer must spend money on marketing to attract consumers to their insurance services, the technology company uses existing consumers. Furthermore, while the traditional insurer is dependent on their revenues from insurance services, the technology company can draw profits from other services and provide insurance without any profit.

Despite some convergence, certain differences are likely to remain even after this transitionary period. This is because the two models have distinct competitive advantages. Traditional insurers no longer monopolize the capability of providing insurance, but they still have the existing user base and utilize it to evaluate risk. Technology-savvy companies that now offer insurance, have their own forms of engagement with their consumers, use different methods to evaluate risk due to their access to real time data, and do not prioritize generating revenue but instead utilize insurance to increase their user base, overcome barriers, and reduce the overall cost of their products and services.

Therefore, when insurers are thinking about how to utilize AI and plot their course through the turbulent, unpredictable times ahead, they should stay true to what they are. This is their comparative advantage.

Dr Alex Zarifis is a lecturer at the University of Nicosia in Cyprus.

This post is adapted from his paper, “Evaluating the New AI and Data Driven Insurance Business Models for Incumbents and Disruptors: Is there Convergence?” available on SSRN.

This article was published on Duke University’s Global Financial Markets Center, a big thank you to Lee Reiners, @leereiners, Kale Wright and Mario Olczykowsky, @m_olczykowski:

My start as a lecturer was rather unusual. Most of the others from my PhD cohort at the University of Manchester progressed seamlessly to lectureships without having to change their topic. My first role was to take several face-to-face modules on different topics, convert them to online modules, retrain the lecturers to teach online and get the programmes validated for online delivery.

This meant I fell behind in my specialisation that was e-commerce and trust, but it gave me an appreciation of the importance of studying different teaching approaches and adapting to different contexts. There is a huge variety of approaches with different advantages. For example, one reputable university has three compulsory assignments per week to ‘force’ students to engage whilst another has one assignment per module to avoid over-assessment.

There are certainly no simple answers or one model that always works. The only solution is to constantly learn different teaching approaches, understand our context and try to marry the two as best we can.

I have tried to understand the impact of context on education for many years. I have researched how collaborative patterns improve online collaboration among students [1] and how to develop a course for cross-border e-commerce [2]. More recently I have explored the potential of Artificial Intelligence in education [3], how to improve student satisfaction online [4] and the impact of online learning for students during the pandemic [5].

When I was doing my PhD, I had a professor that told me I had to read three papers a day. I do not achieve this most days, but it is a clear target for me to aspire towards. I believe a clear target for us to aim for as lecturers is to read one paper or book chapter on education a week. I hope we do not have another pandemic but if we do our homework and improve our craft, we should be ready for whatever new context we face.

References

1. Cheng, X., Wang, X., Huang, J., & Zarifis, A. (2016) ‘An Experimental Study of Satisfaction Response: Evaluation of Online Collaborative Learning’, International Review of Research in Open and Distributed Learning, 17, 60–78. http://www.irrodl.org/index.php/irrodl/article/view/2110 (open access)

2. Cheng, X., Su, L. & Zarifis, A. (2019) ‘Designing a talents training model for cross-border e-commerce: a mixed approach of problem-based learning with social media’, Electronic Commerce Research, 19, 801–822. https://link.springer.com/article/10.1007/s10660-019-09341-y

4. Efthymiou, L., Zarifis, A. (2021) ‘The International Journal of Management Education Modeling students ’ voice for enhanced quality in online management education’, The International Journal of Management Education, 19, 100464. https://doi.org/10.1016/j.ijme.2021.100464

5. Zuo, Y., Cheng, X., Bao, Y., Zarifis, A. (2021) Investigating user satisfaction of university online learning courses during the COVID-19 epidemic period. In: Proceedings of the 54th Hawaii International Conference on System Sciences. pp. 1139–1148 . http://hdl.handle.net/10125/70751 (open access)

Thank you to the University of Nicosia, especially Chara Zymara and Kasiani Pari, for featuring my article:

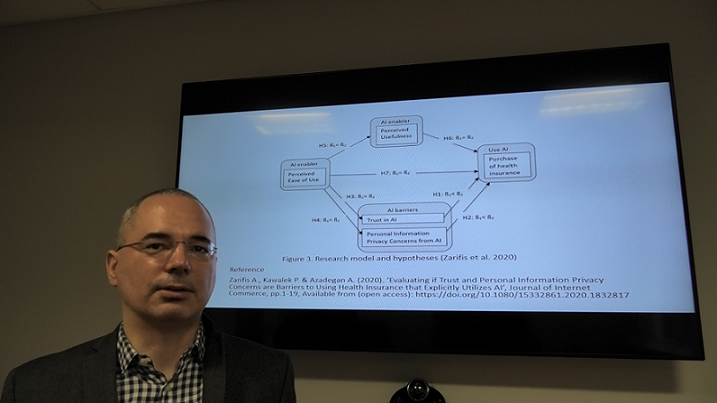

The capabilities of Artificial Intelligence are increasing dramatically, and it is disrupting insurance and healthcare. In insurance AI is used to detect fraudulent claims and natural language processing is used by chatbots to interact with the consumer. In healthcare it is used to make a diagnosis and plan what the treatment should be. The consumer is benefiting from customized health insurance offers and real-time adaptation of fees. Currently the interface between the consumer purchasing health insurance and AI raises some barriers such as insufficient trust and privacy concerns.

Consumers are not passive to the increasing role of AI. Many consumers have beliefs on what this technology should do. Furthermore, regulation is moving toward making it necessary for the use of AI to be explicitly revealed to the consumer (European Commission 2019). Therefore, the consumer is an important stakeholder and their perspective should be understood and incorporated into future AI solutions in health insurance.

Dr Alex Zarifis discussing Artificial Intelligence at Loughborough University

Recent research at Loughborough University (Zarifis et al. 2020), identified two scenarios, one with limited AI that is not in the interface, whose presence is not explicitly revealed to the consumer and a second scenario where there is an AI interface and AI evaluation, and this is explicitly revealed to the consumer. The findings show that trust is lower when AI is used in the interactions and is visible to the consumer. Privacy concerns were also higher when the AI was visible, but the difference was smaller. The implications for practice are related to how the reduced trust and increased privacy concern with visible AI are mitigated.

Mitigate the lower trust with explicit AI

The causes are the reduced transparency and explainability. A statement at the start of the consumer journey about the role AI will play and how it works will increase transparency and reinforce trust. Secondly, the importance of trust increases as the perceived risk increases. Therefore, the risks should be reduced. Thirdly, it should be illustrated that the increased use of AI does not reduce the inherent humanness. For example, it can be shown how humans train AI and how AI adopts human values.

Mitigate the higher privacy concerns with explicit AI

The consumer is concerned about how AI will utilize their financial, health and other personal information. Health insurance providers offer privacy assurances and privacy seals, but these do not explicitly refer to the role of AI. Assurances can be provided about how AI will use, share and securely store the information. These assurances can include some explanation of the role of AI and cover confidentiality, secrecy and anonymity. For example, while the consumer’s information may be used to train machine learning it can be made clear that it will be anonymized first. The consumer’s perceived privacy risk can be mitigated by making the regulation that protects them clear.

References

European-Commission (2019). ‘Ethics Guidelines for Trustworthy AI.’ Available from: https://ec.europa.eu/digital

Zarifis A., Kawalek P. & Azadegan A. (2020). ‘Evaluating if Trust and Personal Information Privacy Concerns are Barriers to Using Health Insurance that Explicitly Utilizes AI’, Journal of Internet Commerce, pp.1-19. https://doi.org/10.1080/15332861.2020.1832817 (open access)

This article was first published on TrustUpdate.com: https://www.trustupdate.com/news/are-trust-and-privacy-concerns-barriers-to-using-health-insurance-that-explicitly-utilizes-ai/

Trust is necessary whenever there is risk. This means it is more important in some contexts than others. While trust has been researched for many decades, it became a more prominent concern with the introduction and expansion of the Internet. The loss of face to face interaction raised the perceived risk and the importance of trust. Once solutions were found, to reduce the risk and build trust, this became a smaller challenge.

Insurtech is another phenomenon where concern about trust is increasingly important so trust must be explored. Indeed, trust emerges as a problem whenever there is a new widely-adopted technology, like blockchain, 5G or AI. For example, chatbots or virtual assistants that utilize AI are widely used to interact with the person purchasing insurance or making a claim (Zarifis et al. 2020). From the consumer’s perspective there are some concerns. It is unclear if they are trusted and how many interactions with the consumer they can replace.

In this blog I outline the possible constituent factors to support trust in Insurtech. I start with the psychology and sociology of trust, then discuss trust in other areas and trust in AI and data technologies. I then draw these issues together to propose a model of trust in Insurtech.

2) The psychology and sociology of trust

There is literature on trust in many different areas such as business, collaboration and education, but the foundations are usually psychology and sociology. Each specific context such as business or more specifically Insurtech bring with them some idiosyncratic twists on the common themes from psychology and sociology.

Each person has a different physiology and experiences that shape their psychological disposition. Therefore, many models of trust start with this variable (McKnight et al. 2002). In most cases, creating a general model of trust that ignores the different individual disposition is hard to support with the data. Having personally tried to explore and validate models of trust I can confirm that it is usually hard to take this variable out and still have a model that is supported by the data. To put it simply, on the one extreme some people’s default approach is to trust while on the other extreme some people’s default is to mistrust. Most of us are somewhere in the middle. Across various contexts, the psychology of trust is similar as it does not come from the context but from the individual. In other words, someone inclined to trust is this way across several contexts.

The sociological factors influencing trust are not as consistent as the psychological ones because they are influenced by the context to some degree. They are however often similar across similar contexts. These factors can come from the broader society or more specific subsets of society more closely related to the specific context. While we are distinguishing between the psychology and sociology of trust, it is important to clarify that these two shape each other over time and this interaction depends on the specific instance of an interaction.

3) Trust in other areas

One prominent model of trust in e-commerce, widely considered to be the seminal paper bringing trust theory into e-commerce and information systems, showed how dispositions to trust combined with contextual factors created trust (McKnight et al. 2002). Once trust was brought into e-commerce and information systems it has been adapted to several contexts, so that it captures the consumer’s perspective accurately. My more recent research on trust has identified that in a multichannel retail environment including physical stores, 2D websites and 3D websites, trust can be built and transferred between channels (Zarifis 2019). Trust in blockchain based transactions like Bitcoin were found to combine those from e-commerce with some specific characteristics of this technology such as the digital currency, the intermediary and the level of regulation and self-regulation (Zarifis et al. 2014).

The examples we have seen so far involve a payment which puts a monetary value at risk. Trust is also necessary in other contexts however where there is no monetary value involved. For example in online collaboration it evolves over several stages and the interaction can be shaped with specific activities to reinforce it (Cheng et al. 2013). Another example where trust is important despite no monetary value being exchange is education. For example in virtual and semi-virtual teams, non-homogenous groups need to be supported more so that they can build and sustain a stable trust (Cheng et al. 2016).

4) Trust in AI and data technologies

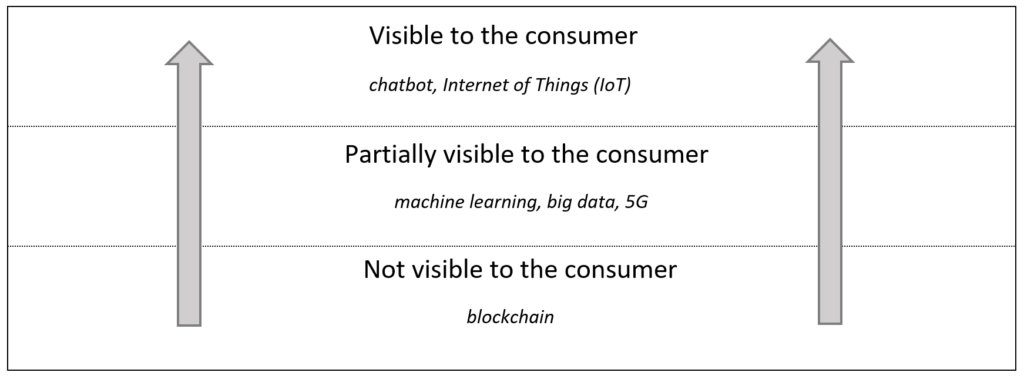

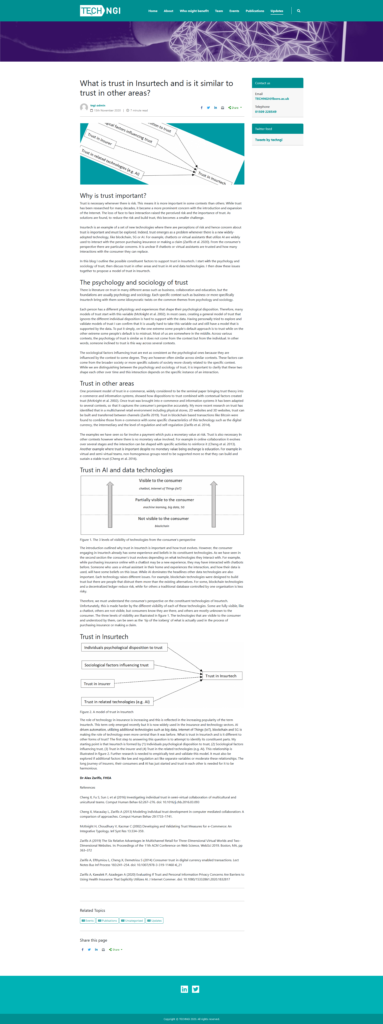

Figure 1. The 3 levels of visibility of technologies from the consumer’s perspective

The introduction outlined why trust in Insurtech is important and how trust evolves. However, the consumer engaging in Insurtech already has some experience and beliefs in its constituent technologies. As we have seen in the second section the consumer’s trust evolves depending on what technologies they interact with. For example, while purchasing insurance online with a chatbot may be a new experience, they may have interacted with chatbots before. Someone who uses a virtual assistant in their home and experiences the interaction, and how their data is used, will have some beliefs on this issue. While AI dominates the headlines other data technologies are also important. Each technology raises different issues. For example, blockchain technologies were designed to build trust but there are people that distrust them more than the existing alternatives. For some, blockchain technologies and a decentralized ledger reduce risk, while for others a traditional database controlled by one organisation is less risky.

Therefore, we must understand the consumer’s perspective on the constituent technologies of Insurtech. Unfortunately, this is made harder by the different visibility of each of these technologies. Some are fully visible, like a chatbot, others are not visible, but consumers know they are there, and others are mostly unknown to the consumer. The three levels of visibility are illustrated in figure 1. The technologies that are visible to the consumer and understood by them, can be seen as the ‘tip of the iceberg’ of what is actually used in the process of purchasing insurance or making a claim.

5) Trust in Insurtech

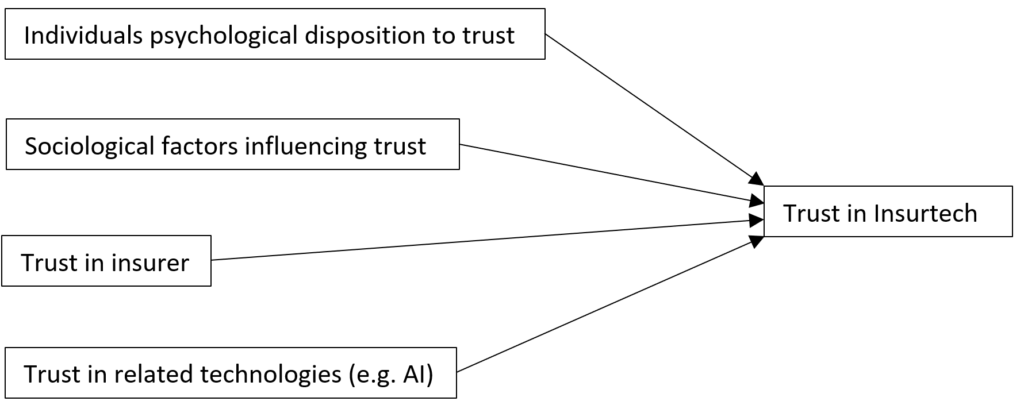

Figure 2. A model of trust in Insurtech

The role of technology in insurance is increasing and this is reflected in the increasing popularity of the term Insurtech. This term only emerged recently but it is now widely used in the insurance and technology sectors. AI driven automation, utilizing additional technologies such as big data, Internet of Things (IoT), blockchain and 5G is making the role of technology even more central than it was before. What is trust in Insurtech and is it different to other forms of trust? The first step to answering this question is to attempt to identify its constituent parts. My starting point is that Insurtech is formed by (1) Individuals psychological disposition to trust, (2) Sociological factors influencing trust, (3) Trust in the insurer and (4) Trust in the related technologies (e.g. AI). This relationship is illustrated in figure 2. Further research is needed to empirically test and validate this model. It must also be explored if additional factors like law and regulation act like separate variables or moderate these relationships. The long journey of insurers, their consumers and AI has just started and trust in each other is needed for it to be harmonious.

References

Cheng X, Fu S, Sun J, et al (2016) Investigating individual trust in semi-virtual collaboration of multicultural and unicultural teams. Comput Human Behav 62:267–276. doi: 10.1016/j.chb.2016.03.093

Cheng X, Macaulay L, Zarifis A (2013) Modeling individual trust development in computer mediated collaboration: A comparison of approaches. Comput Human Behav 29:1733–1741.

McKnight H, Choudhury V, Kacmar C (2002) Developing and Validating Trust Measures for e-Commerce: An Integrative Typology. Inf Syst Res 13:334–359.

Zarifis A (2019) The Six Relative Advantages in Multichannel Retail for Three-Dimensional Virtual Worlds and Two-Dimensional Websites. In: Proceedings of the 11th ACM Conference on Web Science, WebSci 2019. Boston, MA, pp 363–372

Zarifis A, Efthymiou L, Cheng X, Demetriou S (2014) Consumer trust in digital currency enabled transactions. Lect Notes Bus Inf Process 183:241–254. doi: 10.1007/978-3-319-11460-6_21

Zarifis A, Kawalek P, Azadegan A (2020) Evaluating If Trust and Personal Information Privacy Concerns Are Barriers to Using Health Insurance That Explicitly Utilizes AI. J Internet Commer. doi: 10.1080/15332861.2020.1832817

I am very happy and grateful that Loughborough University chose to showcase my research ‘Working from home (WFH): Management styles must evolve to work effectively during the coronavirus lockdown’ on the university website, newsfeed, staff resource page and Imago website, a big thank you to Peter Warzynski and Nadine Skinner:

Working from home (WFH): Management styles must evolve to work effectively during the coronavirus lockdown (9 April 2020)

Managers who are having to adapt and lead virtual teams should adopt a more people-focused style of leadership, according to new research.

Dr Alex Zarifis, of Loughborough University, has published a new paper which outlines the most effective ways of overseeing staff now that most people find themselves logging in from home.

The impact of coronavirus means that face-to-face interactions and office routines are no longer a feature of everyday working life.

This means that the style of management, known as transactional leadership, that until the lockdown had worked successfully, is no longer the most effective way of handling teams.

Instead, says Dr Zarifis, managers should adopt an approach known as transformational leadership – which puts staff member’s needs first.

The main characteristics of this method are:

· Focus on people’s needs, not the tasks

· Focus on motivating and inspiring

· Encourage innovation

Dr Zarifis said: “Transactional leadership focuses on tasks while transformational leadership focuses on people.

“This research found that in challenging times, with a high degree of uncertainty, people focused leadership is better.

“Put simplistically, teams that were forced to become virtual – due to COVID-19 – need a visionary leader, not an administrator.”

He added: “A leader of a virtual team should focus on people’s needs, motivate and be flexible – encouraging innovation.”

The main findings from the paper:

Focus on people’s needs, not the tasks

Understand the situation of each individual and support them in the way they need. If a team member has difficulty working because their children are at home, this would not be within the realms of responsibility of a transactional leader.

But it must be for a transformational leader.

Focus on motivating and inspiring

Accept that monitoring and controlling are often the priorities of functional management and transactional leadership may be less achievable and effective in virtual teams.

Instead act more like a project manager and a transformational leader.

As a transformational leader focus ion motivating and inspiring the shared vision instead of controlling.

What is a shared vision during a COVID-19 outbreak? This could be to stay safe and meet the requirements of our role.

Encourage innovation

Accept that working during COVID-19 is a project and act more like a project manager. A functional manager should accept this change and accept that they cannot act like a transactional manager during this non-routine period and must be flexible.

Managers whose instincts are to control every aspect of the work must learn to take a step back. Instead encourage innovation.

The current context of change must be accepted and utilised.

In the past year, Elon Musk and Tesla have fascinated the world with new innovations like the Tesla Cybertruck. There is excitement about most new Tesla products, but one hugely important one has been largely overlooked. With far less fanfare and no stage performance by Musk, Tesla started offering car insurance last September. In the long run, this is going to have a major impact on most of our lives – perhaps even greater than Tesla’s more eye-catching innovations.

Tesla Insurance is only available for Tesla vehicles in some states of the US at present. It will expand the number of territories gradually over time. But as with the Tesla Cybertruck, the company first wants to see how the business holds up to whatever is thrown at it and whether it cracks under pressure.

For those eligible for Tesla Insurance, the company claims to offer premiums 20% to 30% lower than rivals. Yet even if you are in an area where you can request a quote, Tesla won’t necessarily make you an offer. It sometimes still refers drivers to a traditional insurance partner instead. It may be that Tesla chooses the clearer, less risky cases and sends more complex ones to insurers with more experience and appetite to handle them.

So why is Tesla selling car insurance? For one thing, it has the real-time data from all its drivers’ behaviour and the performance of its vehicle technology, including camera recordings and sensor readings, so it can estimate the risk of accidents and repair costs accurately. This reliance on data may well mean it never branches into selling insurance to drivers of other manufacturers’ cars.

At the moment, Tesla is offering insurance premiums calculated with aggregated anonymous data. In future it could roll out more customised services, like the ones offered by insurers using telematic black boxes, to offer drivers (cheaper) quotes based on how they actually drive.

Every time there is an accident, Tesla has instant access to data about the driver behaviour that led to it. One attraction for the company is that it can evaluate how some of its technologies, like autopilot, stability control, anti-theft systems and bullet-resistant steel, can reduce risk.

Another motivation for Tesla is that some insurers charge a relatively high premium for Tesla cars. One reason is that they still don’t have much historic information about the cost of repairs of electric vehicles. By vertically integrating insurance into its offering, Tesla brings down the price of owning its products.

At the same time, insurance is a barrier to many innovations that Tesla is targeting for the future. With the insurance taken care of, it will be easier to sell self-driving vehicles or send people to Mars (with sister company SpaceX). Like many things Elon Musk does, this both solves a short-term problem and fits the longer-term strategy. It’s a little like how Tesla focused on producing luxury vehicles first to finance the infrastructure for selling cheaper cars like the Tesla Model 3.

How insurance is changing

Tesla has one more reason for offering insurance, which is that the sector is changing: a tech company disrupting it fits the zeitgeist perfectly. My research at Loughborough University has looked into this disruption. I evaluated 32 insurance providers around the world including Tesla and found that artificial intelligence, big data, the internet of things, blockchain and edge computing were all rewiring insurance, both literally and metaphorically.

Broadly speaking, the work of the insurer is shifting from local human expert underwriters to automation driven by big data and AI. The existing industry players that I evaluated essentially fell into three categories. Some had recognised they cannot compete with tech companies. They were focusing on interacting with customers, branding and marketing, while outsourcing everything else to companies with the relevant skills.

Other insurers were trying to add new technologies to their existing business model. For instance, some are using chatbots that apply machine learning and natural language processing to offer live customer support. Yet another group had more fully embraced the new technological capabilities. For example, life insurers like Vitality and Bupa now encourage customers to use wearable monitoring devices to offer them guidance on improving their health and avoiding accidents.

Alongside all these were the new breed of insurers, with Tesla perhaps the best example. Others include Chinese giants Alibaba and Tencent. Just like Apple and Google are making incursions into banking and finance, these are tech-savvy companies with many existing customers who are adding insurance to their portfolio of services. In every case, the capabilities of AI and big data-driven automation have acted as a catalyst.

What it means for drivers

In the short term, Tesla drivers can look forward to insurance that is arguably more seamless and convenient and may well be cheaper – particularly if they clock up fewer miles and drive safely. (Drivers should still compare prices with other insurers: the likes of Progressive and GEICO are among those that insure Tesla vehicles.)

In the longer term, this is a sign that insurance – like banking, road tax and many services – will be driven by real-time data. It will probably change our behaviour for the better. We will probably drive slower, eat healthier food and exercise more – even if libertarians will be uneasy.

This shift will challenge our attitudes towards personal information privacy. Some of us will value the benefits of being open and transparent with our personal information, while others might seek solutions that keep their data with them. Edge computing has potential here, since it allows some data processing to be done on your device so that your personal data doesn’t need to be sent to a central server.

So Tesla and Elon Musk have not just added another revenue stream to their many successful endeavours. They are also helping to fundamentally change the way that we interact with insurance providers. In the future, insurers will be more like a partner on our journey both by car and on foot – both on Earth and beyond.

The article by Dr Alex Zarifis on ‘Why is Tesla selling insurance and what does it mean for drivers?’ was covered by several media including the following: